Mastercard (MA) reported its Q1 results on May 2, 2018. Results were simply astonishing, exceeding investor and analyst expectations. The share price has risen from $180 to $191 after the Q1 earnings. One could argue Q1 results are reflected in the share price, but I think Mastercard still has some room to run for the simple reason that Mastercard is on top of two secular trends. The first one is sustained growth in personal consumption expenses. The second trend is the transition from cash to card payment.

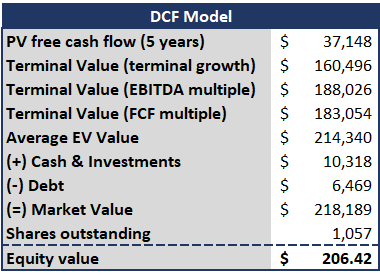

Mastercard is worth $206 based on a DCF valuation which still provides 8% upside versus the current share price of $191.

What happened in Q1Mastercard reported truly terrific results in Q1. Revenue was up 31% or 27% on a currency neutral basis. Revenues, excluding acquisitions and new revenue recognition rules, grew a healthy 20%. The highlight of the quarter was Mastercard��s largest revenue and EPS beat ever. Other highlights include accelerating volume metrics, and new issuer wins (most importantly, Santander's (NYSE:SAN) U.K. debit portfolio, which could increase debit volume by 10%). Underlying operating expenses increased just 12%, significantly less than the 20% revenue growth (Source: Q1 press release). Furthermore, the company bought back 7.9 million shares in Q1, reducing the outstanding share count.

Mastercard confirmed it won the Santander U.K. portfolio. This is important for several reasons. First of all, Mastercard wins the portfolio from Visa (NYSE:V) which is the dominant player in the U.K. Secondly, based on Nilson data, the portfolio could realize of $70 billion in annual volume (Source: JPM analyst report, no link because it is a paid subscription service). The transition adds about 10% to Mastercard��s international debit book and simultaneously reduces Visa��s international debit book by 3%. The conversion is expected to start early in 2019 and phase in over 4 years.

Mastercard is on top of positive secular trendsMastercard is on top of two important secular trends, according to UBS research. The first secular trend is the sustained growth in personal consumption expenditures. According to UBS, people are spending more which is a positive for Mastercard. The second trend is the gradual transition from cash/cheque to card payments, which is really interesting in my opinion. The total worldwide transaction volume is currently about $95 trillion per year. The total transaction volume is divided into $70 trillion cash & cheques transaction volume and $25 trillion in card-based transaction volume. The result is a total addressable market for Mastercard of $95 trillion. Mastercard has an approximate 4% penetration of the total addressable market. The card-based transaction penetration is approximately 17%. The total addressable market is derived from UBS Global Economics PCE, GDP forecasts and data from the Bank for International Settlements (Source: UBS Research).

UBS provided a survey which contained 800 mid-sized businesses in 4 countries (the USA, UK, Germany & France). In these countries, just 70% of the companies accepted Mastercard payments. 94% of the businesses that do not yet accept electronic payment intend to add support for this over the next 12 months. Even in first world countries, not all merchants accept electronic payments. This in itself provides a growth opportunity for Mastercard. I assume the shift towards card payments will continue, and this in turn fuels Mastercard��s revenue growth. The revenue growth is an important factor in the valuation of Mastercard.

Mastercard DCF ValuationMastercard is worth $206 based on a discount cash flow valuation. I use the following inputs for my model.

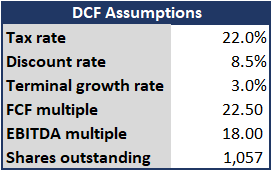

Tabel 1: DCF assumptions

I use a future tax rate for Mastercard of 22%. This is based on the new federal tax rules, with a federal tax rate of 21%. I have added 1% to be on the safe side. I use a discount rate of 8.5% which is widely used in the industry and a terminal growth rate of 3%. I use 3% because my DCF model forecasts 5 years, and I think Mastercard has the moat to grow at 3% thereafter. The terminal growth rate valuation is mostly used by academics to calculate terminal value. Analysts usually use free cash flow (FCF) or EBITDA multiples to calculate the same terminal value. The terminal value is the main contributor to the Enterprise value. Because the terminal value multiples are so important, I didn��t assume these multiples by myself. I screened through several analysts' reports and averaged the multiples used in the reports. The multiples assigned to Mastercard are not uncommon in the industry. Lastly, I used the diluted amount of shares outstanding as of Q1 2018.

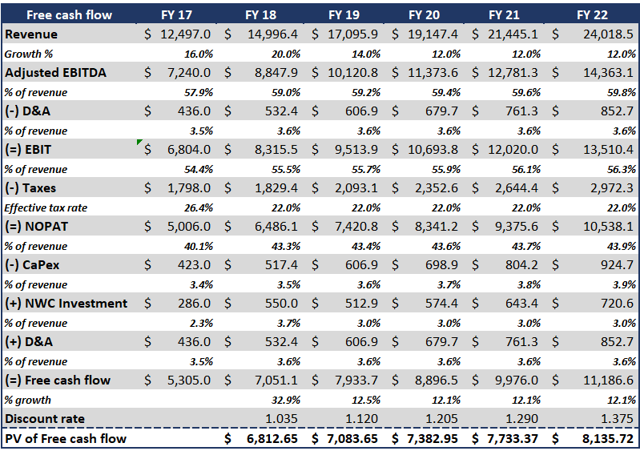

Table 2: Mastercard cash flow forecast

On the revenue front, I forecast 20% revenue growth in 2018 which is in line with guidance provided by Mastercard. I expect the growth to decline somewhat to 12% in FY 2022. I expect the EBITDA margin to increase slowly over the years, primarily driven by the strong revenue growth.

Depreciation and amortization have been quite stable as a percentage of revenues in the last couple of years. Therefore, I forecast D&A as a percentage of revenue in line with previous years. I assume Capex to grow somewhat as a percentage of revenue, mainly to keep fueling revenue growth. I use a discount rate of 8.5%, but I do not fully incorporate the rate in the first year. An 8.5% discount rate in 2018 would mean all cash would flow into Mastercard at exactly 31 December 2018. In reality, cash flows into the company during the year. I correct for this using a discount rate of 3.5% after which I add 8.5% on a yearly basis.

Table 3: DCF Model

The present value of the free cash flow from 2018-2022 is $37.15 million. The terminal value for the terminal growth rate is $160.5 million. The terminal values for the multiples are $188.0 million and $183.0 million. I average the three terminal values and add the present value of the free cash flow from 2018-2022. The result is an average EV value of $214.3 million. The market value is equal to the enterprise value �� debt + cash & investments. The total market value is $218.2 million. The last step is to divide the market value by the shares outstanding to get the equity value. The equity value ends up being $206.42 or $206 when rounded. The DCF valuation has an 8% upside versus the current share price of $191.

ConclusionMastercard reported truly astonishing first-quarter results with the highest revenue and EPS beat in the history of the company. The company is riding the waves of two positive secular trends and has ample room to grow. Mastercard will produce strong cash flow growth fueled by growth in revenue and margin expansion. The value of the company is based on my personal cash flow forecast combined with three models to calculate the terminal value. Based on my model, shares are worth $206 which provides an 8% upside potential.

Disclosure: I am/we are long MA.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment